Government & Regulatory | Top Story

EIA’s “Glut” Calls: The 2025 Surplus Claim — and How 2021–2024 Forecasts Actually Held Up

The “~2.2 MMb/d glut in 2025” framing traces to the EIA’s Short-Term Energy Outlook (STEO), December 2025. EIA doesn’t usually write “glut” in the tables—what they publish is the implied balance via inventories: “world total crude oil and other liquids inventory net withdrawals.” A negative number means inventory builds (supply > demand). In the December 2025 STEO, the 2025 world total is –2.24 MMb/d, which is where the “~2.2” number comes from.

But the better question is the one you’re asking: do these big balance calls hold up when you look back? So below is a clean “forecast vs. reality” check for 2021–2024.

How the back-test works

-

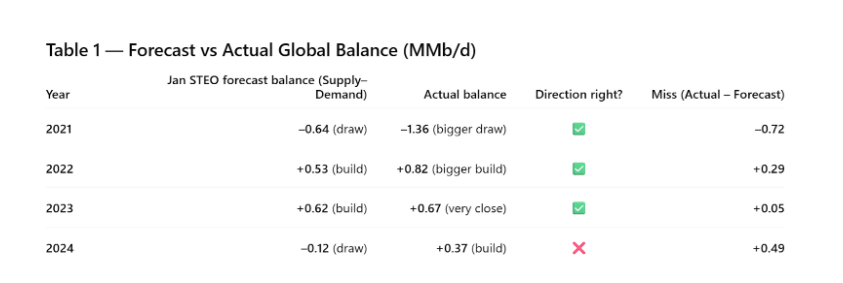

Forecast = what EIA said in the January STEO for that year (their “start-of-year” view)

-

Actual = what EIA later carried as history in the December 2025 STEO dataset

Metric = World petroleum and other liquids supply and consumption, in MMb/d

What this says in plain English:

-

EIA was directionally correct in 2021–2023 (draw, then builds).

-

2024 is the key exception: EIA started the year calling for a slight draw, but the year finished as a noticeable build.

The conclusions you can actually use

1) “Big surplus” headlines are not the main problem — direction flips are

The main credibility hit isn’t a 0.2–0.3 MMb/d magnitude miss. It’s when the call changes sign.

That’s exactly what happened in 2024: EIA began the year calling a slightly tighter market, but it ended as a looser market. That’s the kind of miss that can mislead decision-makers (hedging, capital pacing, inventory strategy).

2) EIA’s forecasts tend to be “smooth” — reality is lumpy

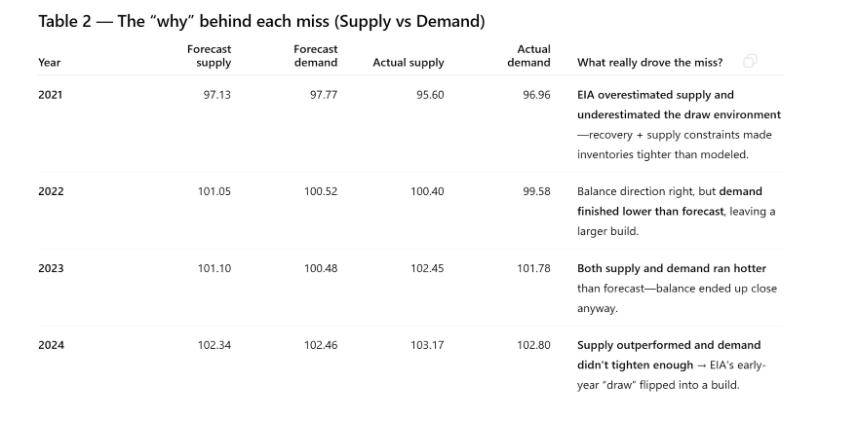

2021 shows the classic pattern: EIA called a draw, but underestimated how tight it would be. When markets are moving through regime shifts (post-COVID recovery, sanctions, OPEC+ discipline), EIA often understates volatility.

3) 2023 is the “best case” example of EIA usefulness

In 2023, EIA’s balance was nearly spot-on even though supply and demand both surprised higher. That’s a reminder: EIA can be very useful when the system is stable and the misses cancel.

4) What this implies for the “2.2 MMb/d glut” in 2025

A projected –2.24 MMb/d build rate is huge—but your back-test shows the right mental model:

-

Treat it as a risk flag (market could be looser), not a certainty.

-

The error bands are large enough that if supply under-delivers or demand over-delivers by ~1 MMb/d, the “glut” narrative can shrink fast.

Related Categories :

Government & Regulatory

More Government & Regulatory News

-

Dallas Fed Energy Survey: What Oil and Gas Executives Are Really Saying

-

MEG Energy Rejects Strathcona Resources' $6 Billion Takeover Offer

-

PDC Energy Second Quarter 2022 Results

-

PDC Energy's 69-Well Kenosha Project Approved by COGCC

-

Biden to Release One Million BPD from Reserves for Six Months; Push for Federal Leasehold Production

Canada News >>>

-

Western Canada Upstream M&A: Q1 2026 Transaction Report

-

A Quiet Capital Pattern Is Forming in North American Upstream — and Almost No One Is Talking About It -

-

Canadan E&P 2026 Program Calls for 448 Net Wells, Up 24% vs. 2025 Plan -

-

Whitecap Details 2026 Duvernay & Montney Program

-

ARC Resources: Lower 2026 Capex, Higher Volumes